The US Health Care System in 2026: An In Depth Overview of Costs Coverage Access and Policy

Introduction

The health care system in the United States is one of the most complex and expensive in the modern world. By 2026 the system continues to evolve under pressure from rising costs, changing policy frameworks, technological innovation, shifting demographic trends, workforce challenges, and ongoing debate about the role of government in health insurance. In this article we explain the major components of the system in 2026 and outline current cost trends coverage patterns access issues quality measures public opinion reform efforts and future directions. This comprehensive review is written with search engine optimization best practices. That means we use relevant keywords like United States health care system costs 2026 insurance coverage policy changes access to care and health care quality.

1. Overview of the US Health Care System Structure

The health care system in the United States is a combination of public programs employer sponsored plans private insurance and out of pocket payments. Major public programs include Medicare which provides coverage for people age 65 years and older and certain disabled individuals, and Medicaid which covers low income adults children pregnant women elderly and people with disabilities. The Affordable Care Act of 2010 created insurance marketplaces where individuals can compare and purchase coverage often with subsidy support. Employer sponsored insurance remains the dominant source of coverage for working adults and their families.

The mix of coverage sources makes health care policy complex. Public and private payers share the largest share of total health care spending. Government pays for Medicare and Medicaid services and private insurers cover a majority of working adults and dependents. Coverage for those without employer plans relies on individual market plans or short term and other private products. Overall the system is pluralistic and fragmented when compared to single payer systems in other industrialized countries.

2. Health Insurance Coverage Landscape in 2026

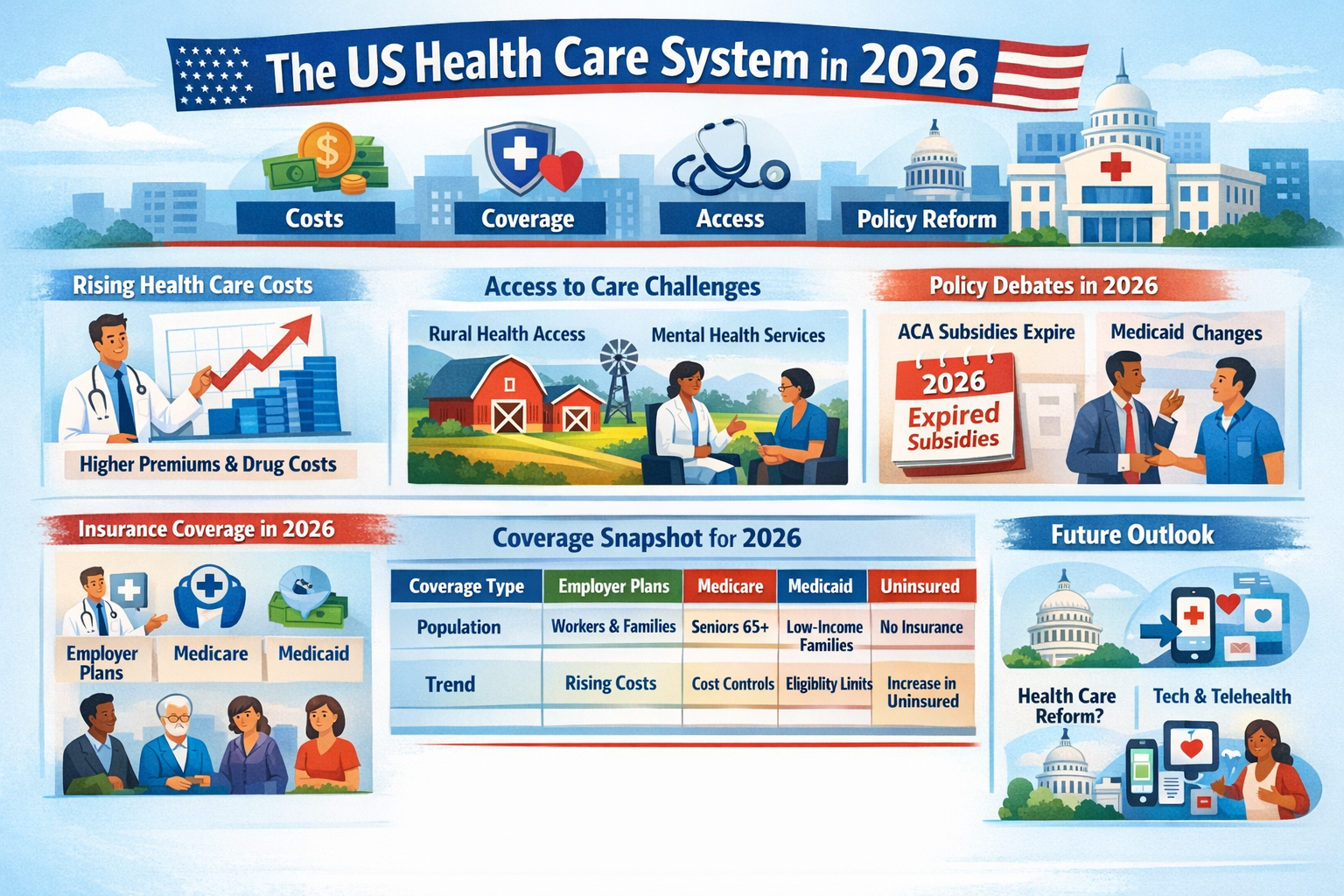

The uninsured rate and coverage patterns in 2026 are substantially influenced by recent policy changes such as the expiration of enhanced Affordable Care Act (ACA) premium tax credits at the end of 2025. Millions of Americans who benefited from reduced premiums saw those subsidies lapse in January 2026, leading to sharp increases in insurance costs and changing enrollment patterns.

2.1 Employer Sponsored Coverage

Employer covered plans continue to cover a majority of working age adults. Employer sponsored coverage remains important for private sector workers. Premium contributions continue to rise for both employers and employees and many companies are adjusting plan designs to manage cost pressures.

2.2 Marketplace Coverage

The ACA marketplaces were expanded with enhanced subsidies during the pandemic which drove record enrollment by 2025. With the expiration of enhanced subsidies at the end of 2025, premium costs rose sharply for many marketplace enrollees at the beginning of 2026. One analysis estimates premium hikes of more than 100 percent for many plans without subsidies. (AP News)

2.3 Medicaid and CHIP

Medicaid continues to be a key source of coverage for low income Americans. Policy changes in the Federal budget reconciliation process have made adjustments to Medicaid provisions with some states implementing stricter eligibility requirements. Research suggests future coverage losses could increase the uninsured population and negatively affect health outcomes. (JAMA Network)

2.4 Uninsured Americans in 2026

Due to subsidy expirations and policy shifts some families may face rising premiums and choose to forgo coverage. Estimates from nonprofit research organizations suggest millions could become uninsured if premium supports remain lapsed.

3. Health Care Cost Trends

Health care costs in the United States are among the highest in the world on both a per person basis and as a share of economic output. Trends in 2026 show continued upward movement, with medical cost inflation being a central concern for individuals insurers employers and government payers.

3.1 National Spending and Cost Drivers

Key drivers of cost include hospital services, physician fees, prescription drugs, administrative expenses, and new high cost treatments. Pharmacy spending in particular continues to grow rapidly and adds pressure to overall cost trends. Another major factor is a rise in behavioral health service utilization.

3.2 Premium Trends

Premiums for employer sponsored plans continue to outpace general inflation and worker earnings growth. Families often pay significantly more each year for coverage while cost of living pressures remain. Premiums vary widely by state and insurer.

3.3 Cost Pressures on the Individual Market

The individual market has experienced volatility with premium increases accelerating as subsidies expire in 2026. Consumers without cost sharing assistance now face higher out of pocket payments and premiums.

4. Access to Care Challenges

Access to medical care is influenced by insurance coverage, provider availability, employment status, and geographic location. Rural areas face systemic access challenges that the federal government is attempting to address through targeted funding initiatives in 2026 with new rural health transformation allocations.

4.1 Rural Health Care Access

Federal funding is directed at improving rural care infrastructure and outcomes. States will receive significant dollars in 2026 under new initiatives designed to reduce barriers and increase care availability outside urban centers.

4.2 Mental Health and Specialty Care

Mental health services are increasingly recognized as essential, but out of pocket barriers persist. Higher costs lead many people to delay or skip needed care which has implications for long term health outcomes.

5. Quality of Care and System Performance

Quality of care in the United States varies by region, provider type, and patient population. While the country leads in many medical innovations it also faces outcomes that lag peer nations. The complexity and fragmentation of the health care system contribute to inconsistency in performance. Continued investment in quality measurement and accountability influences payer and provider behavior.

6. Policy Direction and Reform Debates

Health care policy remains a central issue in national political discussions in 2026. Lawmakers are debating how to address rising premiums coverage gaps cost burdens and disparities in access. Key themes include affordability, sustainability of public programs, role of subsidies, and regulatory changes.

6.1 Subsidy Policy and ACA Marketplace

The expiration of enhanced ACA subsidies is a focal point of congressional debate in early 2026. Political parties differ on whether to extend tax credit supports and how to structure the individual market to stabilize premiums and enrollment.

6.2 Medicaid Policy Proposals

Federal policy proposals suggest Medicaid enrollment losses with stricter criteria. Policy models forecast increased uninsured populations with negative impacts on health outcomes and economic costs. (JAMA Network)

7. Innovation and Technology in Health Care

Technological transformation remains an important element of change in the US health care system. Investment in digital health platforms electronic health records, telehealth services, artificial intelligence for clinical decision support, and data sharing ecosystems aims to improve care coordination and reduce administrative overhead.

8. Comparison of Key Coverage Sources in 2026

The following table provides a snapshot of major insurance coverage types and their characteristics in the United States in 2026.

| Coverage Type | Population Covered | Key Features | Trends in 2026 |

|---|---|---|---|

| Employer Sponsored Insurance | Majority of working adults and families | Large risk pools, shared employer employee premium contributions | Premiums rising, cost sharing increases |

| Medicare | Adults 65 and older plus eligible disabled individuals | Federal program with standardized benefits | Continued coverage with focus on cost management |

| Medicaid | Low income adults children elderly disabled | Joint federal state program | Adjustments to eligibility and implementation |

| ACA Marketplace Plans | Individuals without employer or government coverage | Subsidized plans subject to policy changes | Premiums rising sharply after subsidy expiration |

| Uninsured | Adults and children without insurance | No financial protection for medical care | Potential growth due to cost increases |

Data compiled from government reports and independent analyses of coverage patterns and cost trends in 2025 and early 2026.

9. Public Perception and Satisfaction

Public opinion surveys show a growing number of Americans view the health care system as troubled. Many cite rising costs as the most pressing challenge and express concern about affordability and access. These views reflect ongoing debate about the structure and financing of the US system relative to other developed countries.

10. Key Challenges Facing the System in 2026

10.1 Rising Costs

Costs continue to reflect inflationary factors, pricing variation, technology utilization, and chronic disease burden. Efforts to reduce costs must address provider payment models, administrative inefficiencies, drug pricing, and care delivery transformation.

10.2 Coverage Stability

Instability in policy and support for individual market subsidies creates uncertainty for millions of consumers. Addressing coverage gaps will be central to policy discussions in 2026.

10.3 Health Equity

Disparities persist in outcomes and access to care for racial economic and geographic populations. Policy and program initiatives increasingly focus on equity and targeted interventions.

11. Prospects for Reform

The future of the US health care system remains an open question. Potential reforms include expanding public insurance options, increasing regulatory oversight for pricing and benefit design, and promoting preventative care to reduce long term costs. These efforts reflect evolving public expectations and policy priorities.

Conclusion

The United States health care system in 2026 is at a pivotal point defined by rising health care costs, shifting insurance coverage patterns, legislative debate and performance improvement efforts. Challenges include affordability, access, quality and equity while opportunities for innovation and transformation remain. Understanding these dynamics will help policymakers providers employers and individuals navigate the evolving landscape of health care in the United States.